In late 2023, the Consumer Financial Protection Bureau proposed a rule that would bring large digital payment platforms closer to bank-equivalent supervision. The framing was careful: companies like Apple, Google, and PayPal were not being reclassified as banks, but regulators explicitly raised concern that systems processing payments at massive scale were beginning to function like financial infrastructure without being treated as such.

Apple’s response in its public comment was direct. The company described Apple Pay as a “technology service” that facilitates transactions but does not hold funds or extend credit. Google and Meta used similar language in their filings. Each company maintained the same formal position: they operate infrastructure for commerce, not financial institutions.

At the same time, Apple disclosed in earnings materials that its Services segment — which includes Apple Pay — has grown into a business generating more than $20 billion annually. Amazon, in its shareholder letters and SEC filings, has separately reported billions of dollars in outstanding seller financing through Amazon Lending and affiliated credit programs. These disclosures exist in isolation, but together they point to a structure that regulators are now trying to categorize more precisely than the companies themselves are willing to.

What sits between those two positions is the actual system.

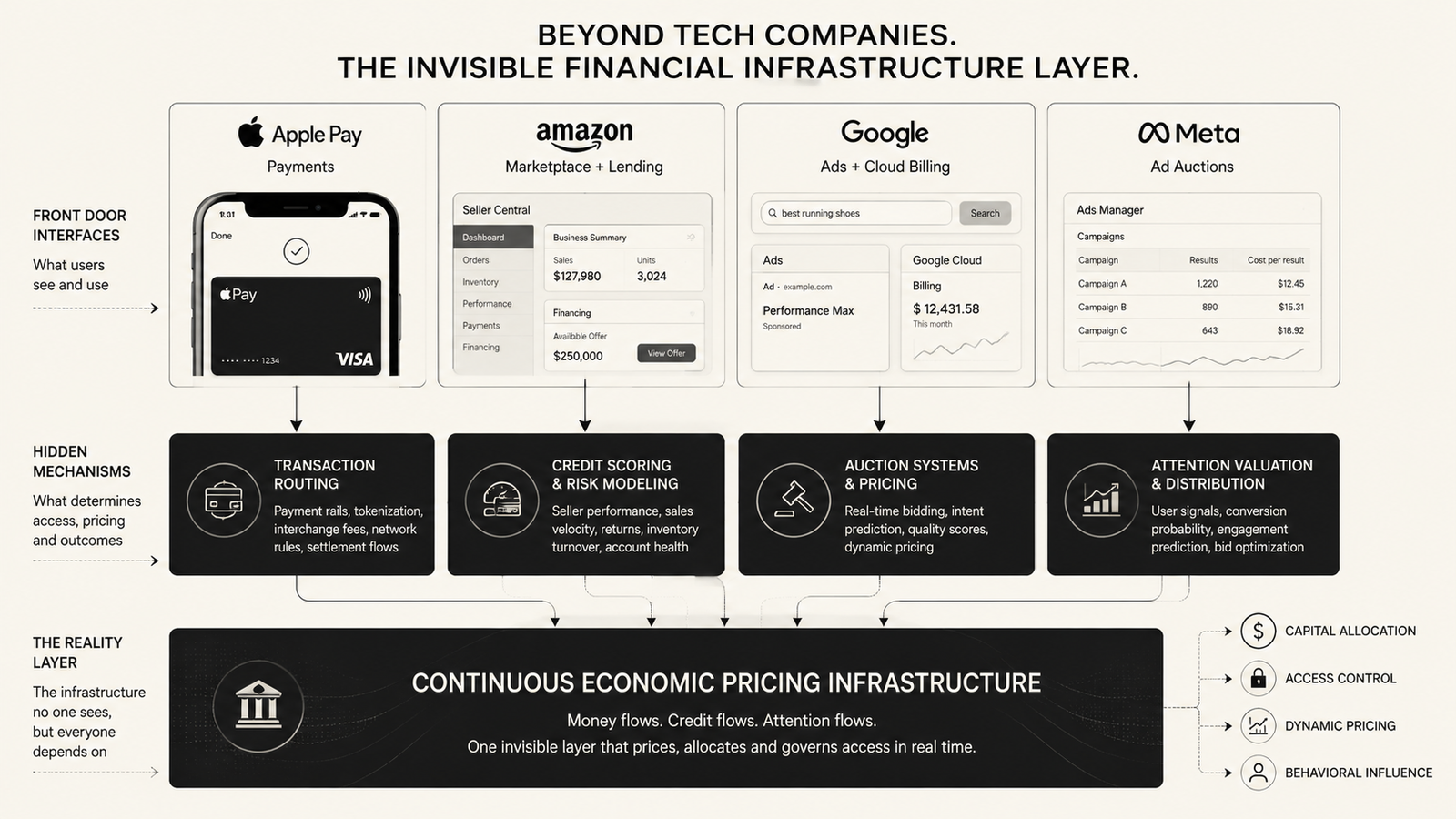

The public framing still separates these companies into familiar categories. Apple is a hardware and software company. Amazon is an e-commerce marketplace. Google is an advertising and cloud provider. Meta is a social platform.

But the operational behavior of these systems no longer fits neatly inside those definitions.

A payment on Apple Pay does not look like banking from the user side. A seller loan issued inside Amazon’s dashboard does not look like credit in the traditional sense. A Meta ad purchase does not resemble a media buy negotiated between advertiser and publisher. A Google Cloud invoice does not resemble a static service contract.

Each of these actions has moved into a system where pricing, access, and eligibility are determined continuously by software models rather than fixed institutional rules.

Apple Pay is the clearest entry point because the scale is visible but the structure is not.

Independent estimates place Apple Pay transaction volume at roughly $6 trillion annually across credit and debit flows. Apple does not process these funds directly in the way a bank would, but it earns a fee on credit card transactions routed through its system. Estimates place this at roughly 0.15% per transaction on credit card usage.

At scale, that structure becomes financially significant. A system most users experience as a convenience layer sits between card issuers, payment networks, and merchants, extracting a small percentage from each interaction while controlling the interface where payment behavior is formed.

In Apple’s earnings calls, Tim Cook has repeatedly referred to Apple Pay as part of a broader “services ecosystem.” The language is deliberate. It avoids classification as financial infrastructure while describing a system that increasingly behaves like one in practice: routing payments, influencing default behavior, and shaping how transactions are completed.

Amazon’s lending system introduces a different layer of integration.

Amazon Lending provides working capital to third-party sellers based on internal performance signals. Amazon does not publicly disclose its full underwriting model, but its seller documentation and SEC filings describe the use of sales history, inventory turnover, and account health metrics in determining eligibility.

External reporting, including coverage from the Wall Street Journal and Bloomberg, has documented how access to financing is often tied to marketplace performance signals that also determine product visibility. Sellers with strong rankings and stable fulfillment metrics are more likely to receive credit offers. Sellers with declining performance frequently lose both visibility and financing access at the same time.

Amazon does not publicly confirm a direct link between ranking systems and lending decisions. When asked in congressional inquiries about the relationship between marketplace algorithms and seller financing, the company has consistently separated “product ranking systems” from “financial services programs” in its responses.

The separation exists in documentation. The correlation appears in outcomes.

Amazon has also reported more than $5 billion in outstanding loans across its seller financing programs. The scale places it in territory that resembles mid-sized commercial lending institutions, though it is not regulated as one.

Google’s financial structure operates through advertising auctions and cloud billing systems that function on continuous pricing models.

Google processes billions of ad auctions per day — estimates place the figure at over 8 billion daily bidding events across search and display inventory. Each auction determines the price of a single impression in real time, based on predicted user intent and advertiser behavior.

This system is not a traditional marketplace in the economic sense. It is a continuously running pricing engine for attention.

At the same time, Google Cloud operates on usage-based billing that meters compute, storage, and API requests at granular levels. The result is a cost structure that behaves less like a fixed service contract and more like a dynamic financial ledger tied to system activity.

Meta’s advertising system completes the same structure from the opposite side.

Meta does not sell impressions in advance. It runs real-time auctions where advertisers compete for behavioral predictions rather than fixed inventory. The system adjusts pricing based on estimated conversion probability, user engagement patterns, and historical advertiser performance.

Internal documentation released during regulatory investigations has shown that ad pricing is not static and can vary significantly across advertisers targeting similar audiences, based on machine-learned predictions about expected outcomes.

Advertisers do not receive full transparency into how these adjustments are calculated. What they see is cost per result shifting without a clear external explanation, even when targeting parameters remain unchanged.

The regulatory layer is beginning to respond to this convergence.

The CFPB’s 2023 and 2024 initiatives explicitly raised concerns that large digital payment platforms were performing financial functions at scale without equivalent oversight. The European Union’s Digital Markets Act introduced requirements for interoperability and transparency in dominant digital platforms, partly in response to concerns about gatekeeping across commerce and advertising systems.

In the United States, the Federal Trade Commission’s antitrust case against Amazon includes allegations that marketplace practices may disadvantage third-party sellers through ranking and visibility mechanisms tied to platform control. While the case is not framed as a financial regulation issue, it directly intersects with how access and pricing are structured inside Amazon’s ecosystem.

These regulatory responses are not treating these companies as banks. They are reacting to systems that increasingly behave like financial intermediaries without being classified as such.

What is less visible in public documentation is what is not disclosed.

Apple does not break out Apple Pay revenue as a standalone line item in its financial reporting. It is embedded within the broader Services category. Amazon does not publish the full variables used in its seller credit scoring system. Meta does not disclose the internal weighting of factors that determine ad auction outcomes. Google does not provide detailed breakdowns of how individual query-level auction dynamics translate into aggregate pricing changes.

These omissions are not unusual in themselves. What matters is their consistency across systems that now influence capital access, revenue distribution, and visibility at scale.

In several congressional hearings, Amazon representatives have been asked whether seller ranking systems influence lending decisions. The company’s responses have remained structured around separation of teams and functions, without addressing whether shared data signals influence both systems.

The absence of a direct answer becomes part of the structure itself.

For a third-party seller on Amazon, the system is experienced as a sequence of linked dependencies. A change in product ranking can affect sales velocity. Sales velocity affects eligibility for financing. Financing affects inventory capacity. Inventory capacity feeds back into ranking performance.

For a startup using Google Cloud, infrastructure cost is not fixed. It responds to usage patterns, scaling decisions, and architectural choices that are continuously priced.

For an advertiser on Meta, acquisition cost is not stable across time. It shifts based on auction dynamics that are not fully observable from the outside, even when inputs remain unchanged.

These are not isolated systems. They are interconnected operational environments where access to capital, visibility, and infrastructure is mediated through software-controlled pricing layers.

The regulatory classification gap sits at the center of the tension.

Financial institutions are typically defined by custody of funds, credit issuance, and systemic risk exposure. These companies formally avoid those categories by structuring their services as platforms, marketplaces, or infrastructure providers.

But in practice, each one now performs partial functions of financial systems: pricing risk, allocating capital, and mediating access to economic activity.

The classification problem is not theoretical. It determines which oversight rules apply, how transparency is enforced, and what obligations exist around disclosure and fairness.

There is a structural contradiction inside this arrangement.

Each system reduces friction for participation while increasing dependence on platform-controlled mechanisms for access.

Apple Pay removes steps from payment flows while consolidating transaction routing through a controlled interface layer. Amazon Lending expands credit access for sellers while tying eligibility to internal performance systems. Google Cloud lowers entry barriers for infrastructure while making long-term cost exposure dependent on usage-based pricing systems. Meta reduces distribution friction for advertisers while shifting cost formation into opaque auction dynamics.

The same design pattern appears across systems that are not formally coordinated but operate under similar incentives.

What ties these systems together is not ownership of money in the traditional sense.

It is control over the conditions under which money moves.

That control is exercised through pricing systems embedded in software infrastructure: transaction fees, ad auctions, usage billing, credit scoring models, and marketplace ranking algorithms.

Each system operates independently, but together they form a layer where economic activity is increasingly mediated by continuous pricing mechanisms rather than static institutional rules.

At a regulatory level, this creates a mismatch that is still unresolved.

Companies respond to oversight using legacy categories that separate technology from finance. Regulators increasingly describe behaviors that resemble financial infrastructure without formally reclassifying the entities involved.

The gap between those two positions is still open.

It is visible in filings, earnings reports, enforcement cases, and disclosures that treat the same systems as either software platforms or financial intermediaries depending on context.

What has not stabilized is the category that connects them.

The clearest observation is not that these companies are becoming banks.

It is that the infrastructure determining how attention, capital, and access are priced is now concentrated inside systems that do not identify themselves as financial institutions.

And the most revealing detail sits in the documentation gap itself: the parts of these systems that determine pricing, eligibility, and access are precisely the parts least likely to be described in full public detail.